The Home Depot Store patty_c/iStock Unreleased via Getty Images

Description

The Home Depot Inc. (NYSE:HD) is the world’s largest home improvement retailer based on net sales (2021 revenues were US$151B). The company operates 2,317 warehouse-style stores (“big box formats”) offering more than 30,000 products in store and 1 million products online in the US, Canada and Mexico.

The company’s product categories include a wide range of building materials, home improvement products, lawn and garden products, décor products and provides several services including home improvement installation services and tool and equipment rental.

The Home Depot opened its first stores in Atlanta in 1979 and went public in 1981. The company has grown revenues primarily organically by opening more store locations (in recent times this is now down to less than 10 per year) with a few relatively small acquisitions and divestments along the way (all in the MRO segment).

In 2007 the HD Supply division was sold to private equity interests who refloated the business in 2013 with an initial public offering. In late 2020 Home Depot repurchased all the public shares of the business for $US 8,692M.

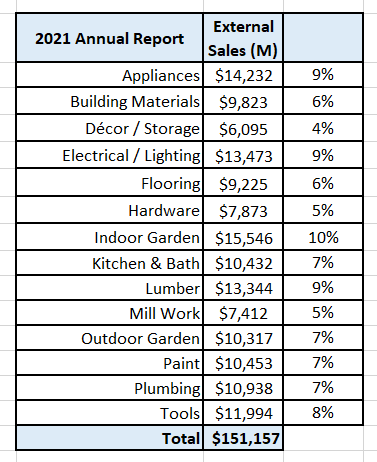

The company has one reportable operating segment but does break-down sales by product category (without providing category profitability):

Author’s compilation

US revenues account for almost 92% of total sales and this ratio has been reasonably constant for the last 5 years. Home Depot is predominantly a US domestic business in the Consumer Cyclical sector.

Business Overview

According to one of the founders of The Home Depot, Bernie Marcus, the company’s original market strategy was to provide the most complete assortment of lumber, building materials and home improvement products, competitively priced in a service-oriented retail situation.

It is fair to say that current management has remained true to the original strategy and the company has continued to innovate and continuously improve its offerings and service performance.

Addressable Market In The United States

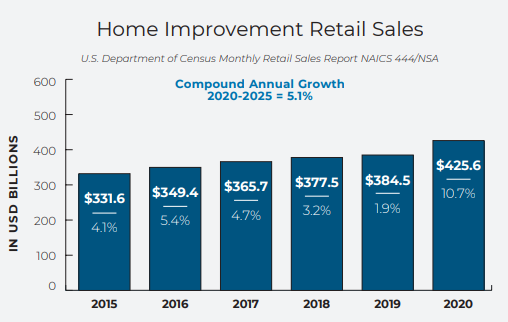

The historical US retail market for home improvement products is shown on the following chart:

Based on the reported sales growth of the major sector retailers, Home Depot and Lowe’s, the market may have grown by a further 8% to 10% during 2021.

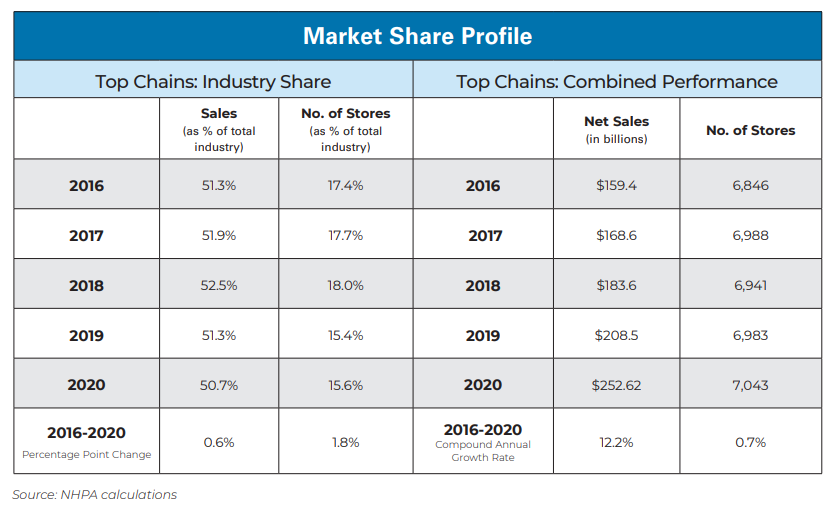

According to the North American Retail Hardware Association the sector is very fragmented but is dominated by the “big box” retailers which includes Home Depot, Lowe’s (LOW), Tractor Supply (TSCO) and several privately owned companies including Menards Inc, 84 Lumber, Northern Tool & Equipment and Carter Lumber Company. The following chart demonstrates the current situation:

It is noted that this sector has done very well during the COVID-19 pandemic. Due to the various restrictions imposed by government on work and travel and courtesy of the transfer payments made by government to consumers there has been an enormous surge in sales.

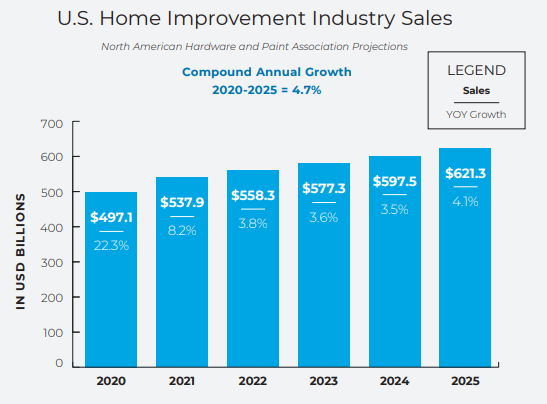

Prior to the pandemic sector sales had been growing by just under 4% per year. Sector revenues grew by approximately 10% in both 2020 and 2021. The question now remains to what levels will future growth in the sector return to?

The consensus estimates for future sector sales growth from various researchers is between 4% to 5% per year through to 2026. This is shown in the following chart:

Although the charts that I have presented so far don’t demonstrate it, the sector’s revenues have historically been quite cyclical. Since the economic recovery which has taken place since the global financial crisis (GFC), the sector has performed reasonably strongly and has not experienced a down year.

Many of the projections for the sector’s future growth are now becoming a little dated and more recent deteriorating economic conditions may have cause to temper the sector’s near-term growth projections.

Maintenance, Repairs And Operations (MRO)

Home Depot’s management have waxed and waned over the years regarding this segment. It is currently viewed positively as a means to extend the company’s addressable market following the acquisition of HD Supply in 2020.

Long-term investors will recall that HD Supply was at one time a division of Home Depot and it was sold to private equity interests in 2007. Interestingly HD Supply was sold for $8,300 M in 2007 and re-acquired for $8,692 M in 2020.

According to Grandview Research, the US MRO market size is approximately $143 B. The segment is thought to be mature and growing at around 2.5% per year. The MRO market is quite diversified, and HD Supply does not participate in all the markets within the segment.

Home Depot has recently stated that the addressable MRO market for their HD Supply business is about $100 B in size. It is noted that HD Supply’s revenues in the year before its acquisition were $6,146 M which equates to a market share of just over 6%.

International

The Home Depot has expanded its reach internationally through a relatively small acquisition in Canada in 1994. Today the company has expanded organically to 182 Canadian stores. In 2001 the company acquired its first Mexican store and today has 129 stores. However not all the international expansions have been successful. In 2006 the company acquired 12 stores in China but by 2012 they were all closed with a “clash of cultures” being slated as the reason for The Home Depot format not working in China.

In 2021 international sales represented 8% of total net sales revenues. The proportion of international sales has been unchanged since 2016.

Home Depot’s View Of The Addressable Market

Home Depot claimed in their 2021 4th quarter market release, management considers the company’s addressable market to be $900 B in size. For the first time this estimate includes the relevant Canadian and Mexican markets.

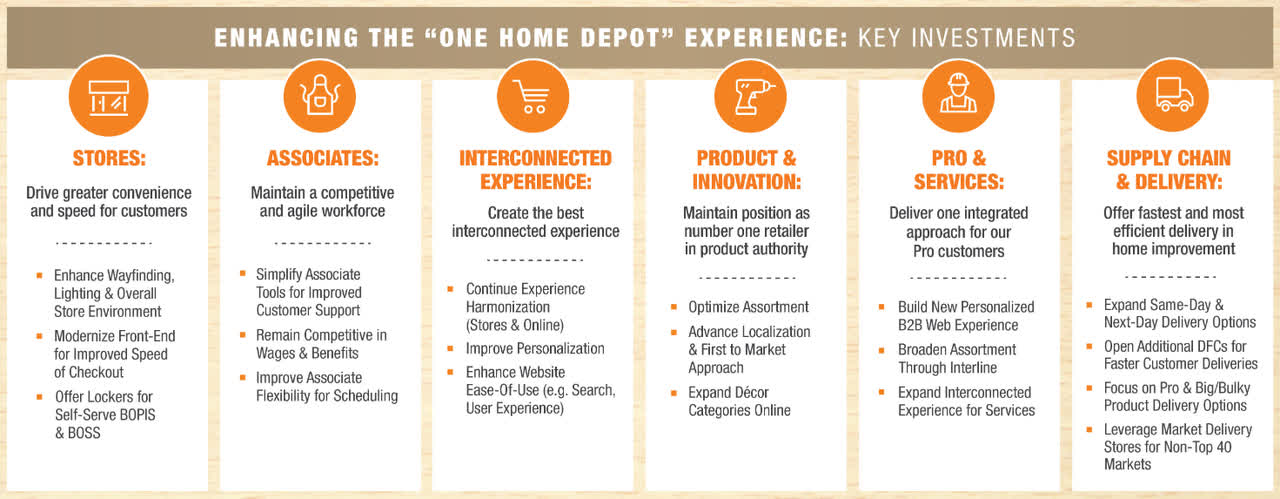

The Home Depot Strategy

In 2017 the company announced a new strategic initiative to kick start the next phase of growth – called One Home Depot. This multi-year strategy, which is still active, is designed to further enhance the customer experience (both digitally and in-store). The strategy is summarized on the following company chart:

On balance this strategy appears to be an extension of the company’s long-term strategic approach focusing on customer service, product knowledge and innovation in both product and service.

Home Depot has not provided any significant strategic updates due to COVID restrictions. The last Investor’s Day presentation was in 2019.

How has the strategy been working so far?

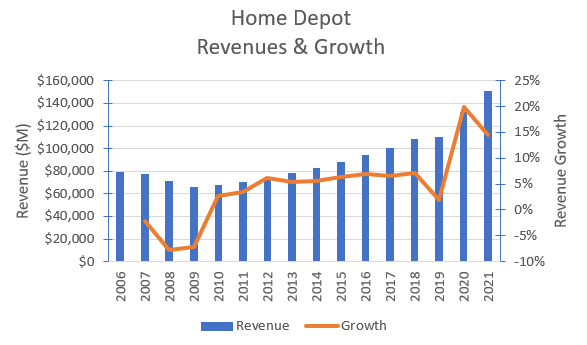

The following chart shows Home Depot’s revenues and revenue growth since 2006:

The chart shows that revenues bottomed during the GFC in 2009. After the GFC revenues grew reasonably consistently at 5% to 7% year on year until the year before the onset of the COVID pandemic. Home Depot and its major competitor Lowe’s did extraordinarily well during the COVID lockdowns.

I would conclude that the Home Depot strategy is working well.

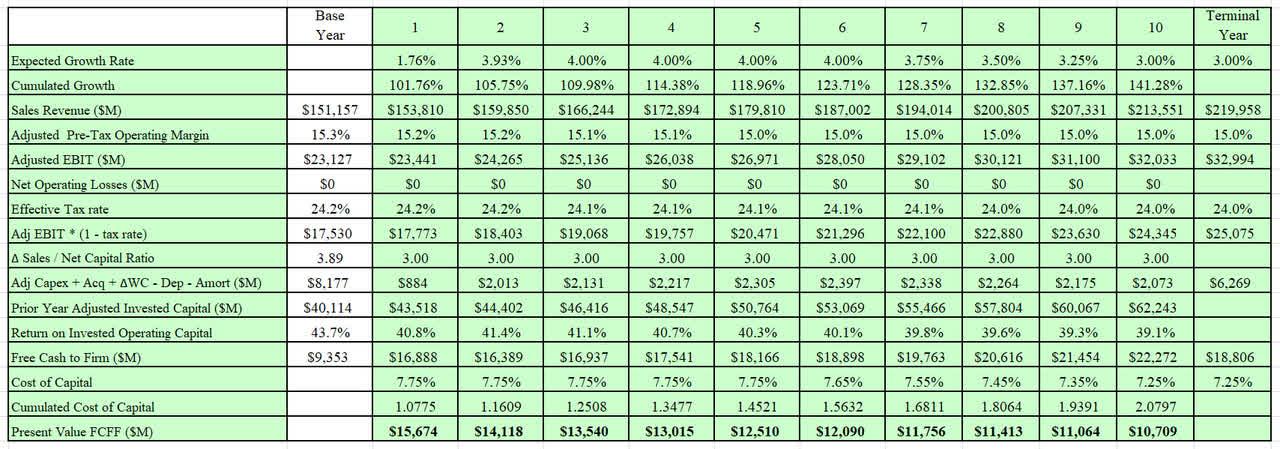

The Home Depot’s Historical Financial Performance

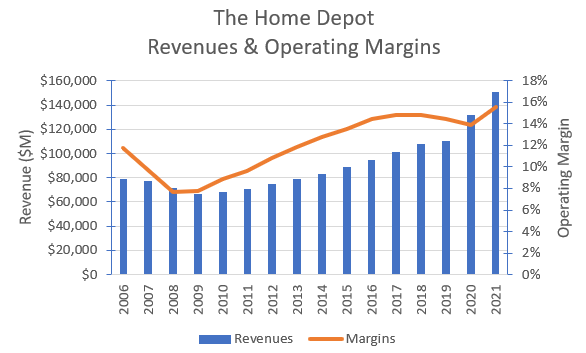

The Home Depot’s consolidated historical revenues and adjusted operating margins are shown in the chart below:

It should be noted in 2019 there were changes to the way the accounting standards treated operating leases. I have made manual adjustments to Home Depot’s historical financial accounts in order to ensure consistency with the current financial statements.

The chart shows that Home Depot has successfully grown revenues and margins since the GFC. The company suffered a reduction in margin during the early stages of COVID, but they have since recovered these costs and margins are currently at the highest reported levels for more than 15 years.

I recently completed an analysis of the 350 largest listed cyclical retailers in the world. The current median operating margin for this sector is 7.2% and the 75 th percentile is 13.0%. This suggests that Home Depot’s operating margins are in the highest quartile for the sector.

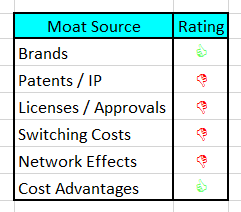

The Home Depot Moat

My moat assessment for The Home Depot is shown in the following table:

The sources of The Home Depot moat are:

- Its excellent brand which is well respected by its customer base.

- The cost advantage it gains from its suppliers by virtue of its scale.

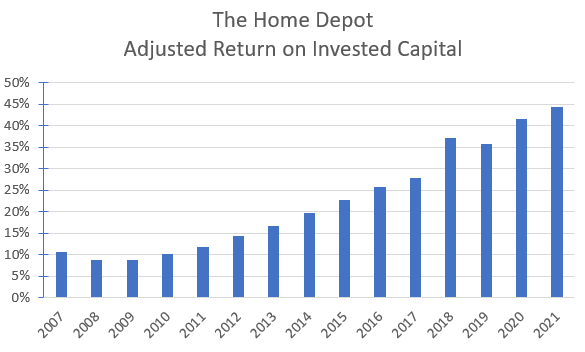

Compared to its competitors I believe that The Home Depot’s moat may be wide and deep. This is supported by the company’s return on invested capital (ROIC) which is shown in the chart below:

The chart shows the spectacular improvement in the ROIC that has taken place since the GFC.

This is an excellent result. Typical ROIC for cyclical retailers is 10% and Home Depot’s current ROIC is in the highest decile for the sector.

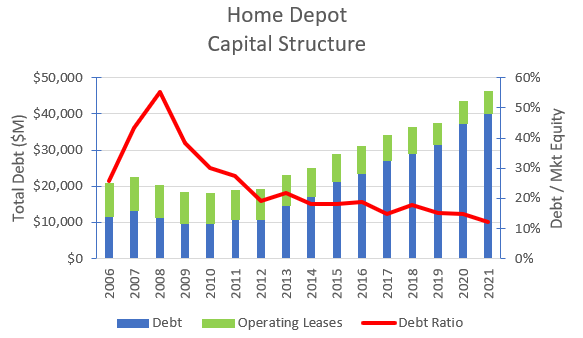

Home Depot’s Capital Structure

The following chart shows the history of Home Depot’s capital structure:

Home Depot has been steadily reducing its debt ratio since the GFC. Typical cyclical retailers currently have a debt ratio of 26%. Home Depot’s debt ratio is in the sector’s lowest quartile.

The data would suggest that Home Depot’s balance sheet is very strong and the company is well positioned to be able to apply additional leverage to its balance sheet if the opportunity arises.

Home Depot’s Cash Flows

A key metric that I check with every company is a comparison of the reported Net Income versus the Net Operating Cash Flow:

I have no concerns about Home Depot’s financial statements.

A company which consistently reports net operating cash flows exceeding net income gives me a higher level of comfort that the Income Statement is not being periodically adjusted to boost earnings.

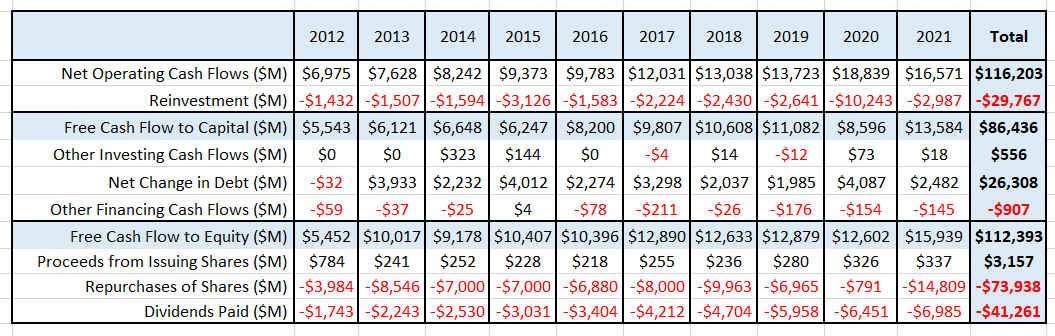

The following table summarizes Home Depot’s cash flows for the last 10 years:

The data indicates that over the last 10 years Home Depot has used 4 main drivers to increase its ROIC:

- It has grown revenues at a CAGR of 7.9%.

- It has increased adjusted operating margins from 10.9% to 15.6% predominantly through operating leverage (gross margins have slightly declined).

- It has had the benefit of a lowering of its effective tax rate from 37% to 24% because of changes to the US tax code.

- It has increased its capital efficiency through a combination of dividend payments ($41,261 M) and net share buy-backs ($70,781) whilst increasing leverage by $26,308 M.

Recent Share Price Action

The chart indicates that it has been a difficult 12 months for Home Depot. There has been considerable volatility in the stock’s price. For large parts of the year the stock has significantly under-performed the S&P 500 index.

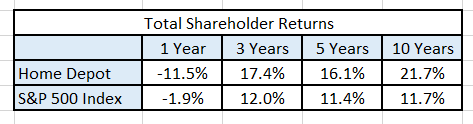

Historical Stock Returns

The data indicates that Home Depot has been a wonderful investment for a long period of time and has easily outperformed the general market until recently.

Key Risks Facing Home Depot

I think that there are relatively few long-term structural risks facing Home Depot given that the underlying market for its products are both mature (based on long-term demographics) and cyclical (particularly sales to home builders).

The near-term performance of the company will be heavily influenced by macro-economic conditions and issues associated with the performance of its supply chain (particularly products whose production has been impacted by COVID disruptions). Supply chain inflation should be able to be passed through to customers, but this may contribute to a general lowering of demand.

Supply chain risks associated with China are not considered a major concern over the medium term. According to a JP Morgan 2019 research note, approximately 16% of Home Depot’s products are sourced from China.

I suspect that the risks of significant challenges to the company’s preeminent position in its sector are relatively low. I also suspect that the company’s supplier base is also not able to jeopardize its market position.

The remaining risks are within the company’s control and relate to strategy execution. Could the company lose its way strategically by changing the fundamentals of its offering or through a series of poor investments/acquisitions? How will the company attempt to maintain its growth trajectory? Will it place more emphasis on international expansion, or will it attempt to acquire a new product vertical within the US?

These risks are real. The company has recently had a change of Chief Executive Officer following the retirement of Craig Menear after 7 years in charge which always increases the risk of a change in strategic direction.

But the company’s track record over many years has been excellent, so I suspect that these risks are also relatively low.

My Investment Thesis for Home Depot

At the time of writing this report the company’s consensus revenue forecast for 2022 was 1.8% higher than 2021 actuals and it is projected that 2023 revenues will increase by 3.9% over 2022.

This would indicate that the analysts believe that the “COVID bump” that Home Depot received is over and that future revenue growth is once again in line with the pre-COVID trend.

Due to its size, I think that it will be very difficult for Home Depot to grow faster than its underlying market in the US. Similarly, the underlying market growth rates in the international markets may be a little lower than the US but there are more opportunities to gain market share in these markets. Any market share growth in Canada and Mexico would come at the expense of margins as share would need to be “bought”.

Home Depot’s operating margins have been slowly rising for many years and are now in the top quartile for the sector. I suspect that given the economic headwinds which are coming I don’t believe that margins can continue to increase and will flatten out from here.

Although pressure may build to make investments to extend the company’s reach into adjacent markets or new countries in order to extend the company’s growth trajectory, I expect that management discipline will prevail and this will be resisted. As a result, I have not factored in any major acquisitions. This means that the company may be able to reduce its rate of capital spend over time.

As Home Depot settles into a lower growth situation then the capital structure can be adjusted to take on more debt. This will shift the debt ratio closer to the median levels of the sector. This will lower the company’s cost of capital and release additional capital for distribution back to shareholders.

Valuation Assumptions

In summary, this should enable Home Depot to achieve:

- Revenues will grow at 4% ± 2% for the next 5 years before growth begins to decline to GDP (3.0%) at the end of year 10.

- Adjusted Operating Margins will remain at 15% ± 1% into perpetuity.

- Capital productivity (as represented by Δ Sales / Net Capital) will decline from the current level of 3.5 and settle at 3 ± 0.5 (around about the 75th percentile of companies in the Sector).

- The current Return on Invested Operating Capital (around 44%) will decline over time before settling at 12% ± 1% in perpetuity which reflects the enduring moat around business model.

- I have used the Capital Asset Pricing Model (CAPM) to estimate the current cost of capital to be 7.75% and I expect that the mature cost of capital will be 7.25% ± 0.25% (this reflects the low uncertainty associated with The Home Depot’s future revenues and is about the median of the sector).

- I have valued the Management Options at $480 M using a Black-Scholes model.

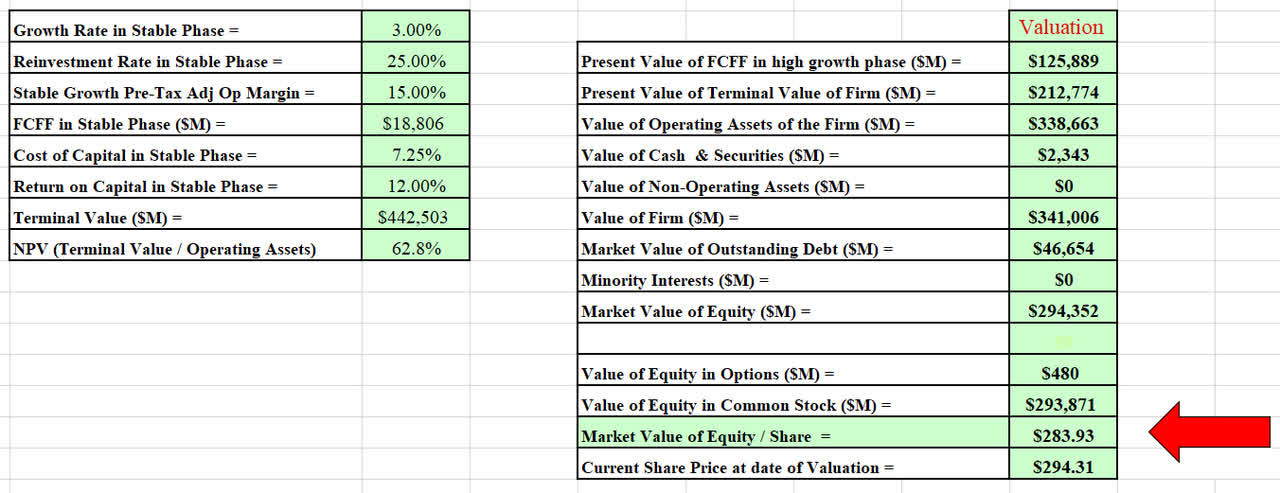

Discounted Cash Flow Valuation

The valuation has been performed in $USD:

The model estimates The Home Depot’s Enterprise Value is $341,006 M and the Equity Value is $293,871 M.

This equates to a mid-point value per share of around $284.

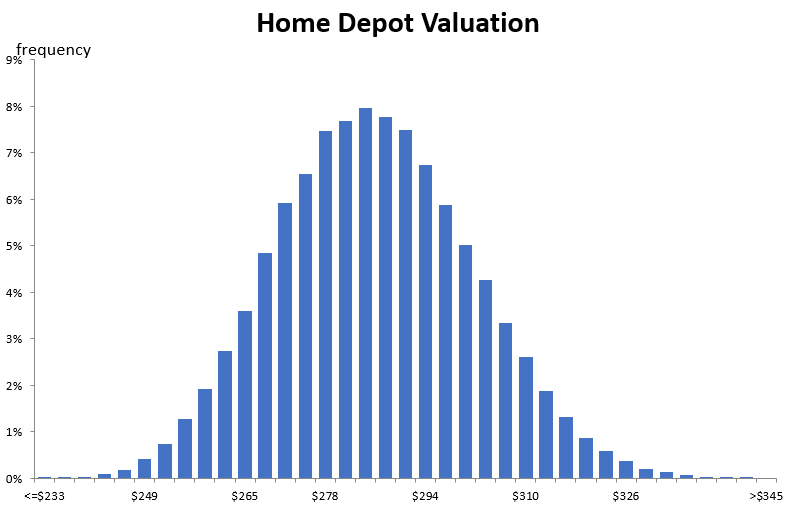

I also developed a Monte Carlo simulation for the valuation based on the range of inputs for the valuation. The output of the simulation is developed after 100,000 iterations.

The Monte Carlo simulation can be used to help us to understand the major sources of sensitivity in the valuation. The valuation’s distribution is mainly influenced by the estimate for sales growth over the next 5 years.

The simulation indicates that at a cost of capital of 7.25% – the valuation for Home Depot is between $233 and $345 per share with a typical value around $284.

This would indicate that Home Depot is currently fairly priced.

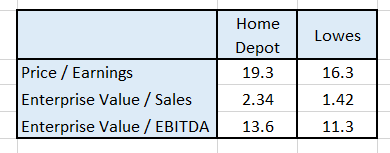

Home Depot or Lowe’s

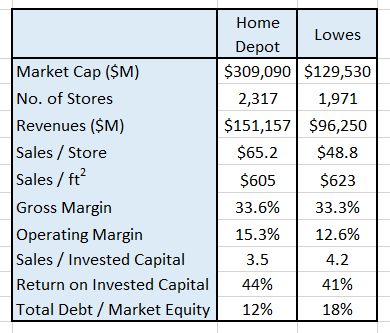

The US home improvement sector is dominated by Home Depot and Lowe’s. Comparing the financial and operating metrics of these 2 companies:

I have performed this high-level comparison many times over the years. Historically Home Depot has always had the superior metrics, but the gap is now closing.

Home Depot is clearly the bigger company and its typical store has a bigger footprint but both companies generate similar revenues per square foot of retail space and have similar gross margins. The key difference is that Home Depot by virtue of its size generates more operating leverage and this is reflected in the higher operating margin. Importantly both companies have a similar return on invested capital.

I have generally felt that Home Depot was the higher quality company from an investment standpoint, but I am now more agnostic about this. Either company would be a worthwhile holding in an investment portfolio.

Although I do not place a lot of significant on relative valuation metrics as a method to identify whether companies are appropriately valued, I note the following table:

My analysis indicates that Home Depot is currently fairly priced. The table indicates that Lowe’s may represent cheaper relative value.

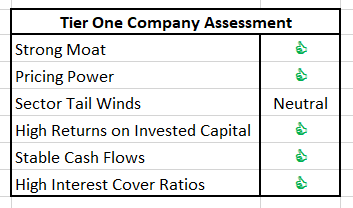

Final Recommendation

For each company that I value I assess what role this company could potentially play in my portfolio. The cornerstone of my portfolio is what I term “Tier 1” companies. These are the companies that I tend to hold for the long term and where I invest most of my cash.

My high-level assessment for Home Depot is:

Clearly, Home Depot is an excellent company and at the right price would be an excellent addition to anyone’s portfolio. As the company is currently fairly priced, I think that the company is a HOLD.

I currently don’t own Home Depot but I expect that over the coming months I will get the opportunity to buy it at a significant discount to its intrinsic value. I intend to buy aggressively when this happens.

More Stories

Best Essential Holiday Decor – Maison de Pax

Insulation FAQ: What is Blanket Insulation

How to Unlock the Bedroom Door?